Summer is shifting into fall, and winter won’t be far behind, followed by the holidays and the New Year – and already, investors are thinking about finding the best stocks to shape up their portfolios for 2024. Meanwhile, the analysts at Goldman Sachs have been busy curating their ‘top picks’ for the coming year.

Goldman Sachs’ Top Picks give investors a useful pointer toward solid stock choices, but they aren’t the only one. Another comes from the Smart Score, an AI-driven, algorithm-based data collection and collation tool that does the leg-work of gathering, sorting, and analyzing the wealth of raw information generated in the markets. Each stock is given a score, a simple single-digit score showing how the stock measures up against a composite of 8 factors known to predict future gains. A ‘Perfect 10’ from the Smart Score indicates a stock that is worth a closer look.

When these ‘Perfect 10′ Smart Score stocks align with Goldman Sachs’ Top Picks, it creates a compelling signal that the average investor can’t afford to overlook.

With that in mind, let’s take a look at a few of those tickers – ones that have earned a spot on Goldman Sachs’ Top Picks list and nailed a ‘Perfect 10’ on the Smart Score.

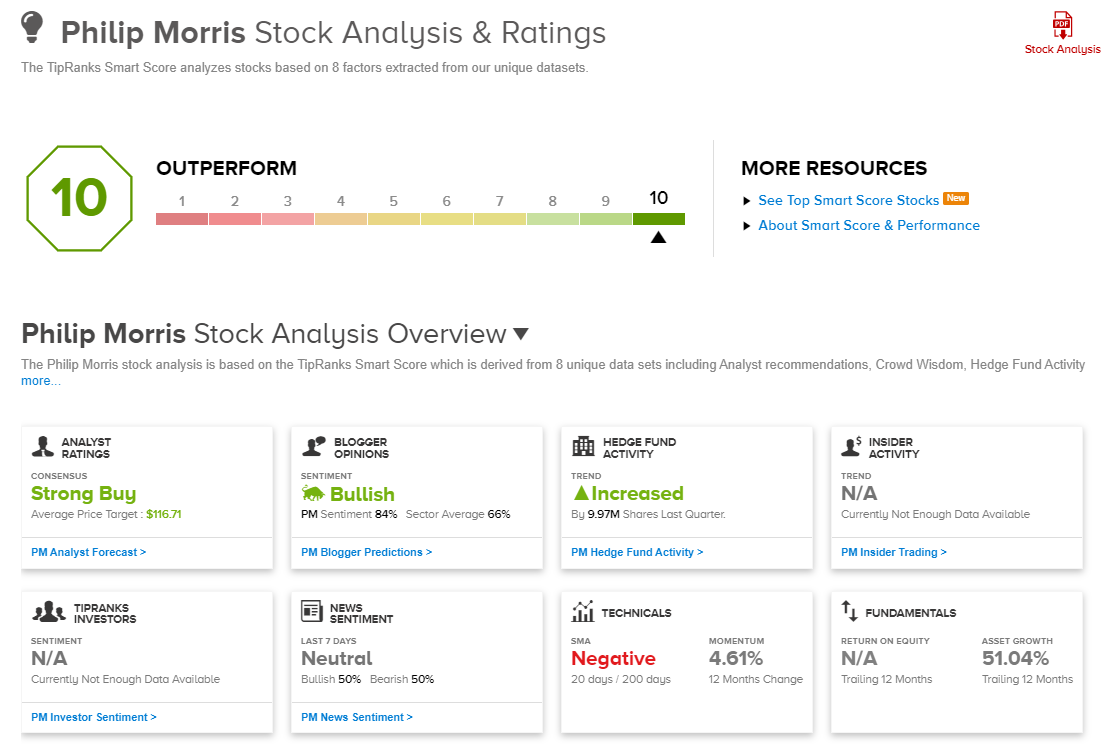

Philip Morris International (PM)

We’ll start with a classic ‘sin stock,’ the tobacco company Philip Morris International. Philip Morris has long been a leader in its industry, and has a headline asset – the full rights to produce and market the Marlboro brand, one of the world’s largest cigarette brands, in the international markets. The company also owns the Next, Chesterfield, L&M, and the eponymous Philip Morris brands. PM is positioned in more than 175 markets around the world, and boasts of holding first- or second-place market shares in most of them.

The tobacco industry was valued at over $867 billion last year, and despite social pressures against it, it is expected to expand to $1.05 trillion by the end of this decade – so Philip Morris’s market-leading positions are no small potatoes. The company is working hard to maintain its position, and adapt to the social trends, through moves toward new products. PM has, over the past several years, put more than $10.5 billion into developing and expanding smokeless tobacco products. This is an expanding market for Philip Morris, which saw smokeless non-nicotine products make up 29.1% of its total revenue in 2021, and 32.1% in 2022.

The company’s efforts – both in its smokeless and ‘traditional’ product lines – have been paying off. Philip Morris realized net revenues of $9 billion in 2Q23, up 14.5% year-over-year and beating the forecast by $259.5 million. At the bottom line, PM reported an adjusted diluted EPS of $1.60, showing a near-17% y/y gain and coming in 12 cents ahead of the forecasts.

Keeping all of that in mind, Goldman has taken a bullish view of Philip Morris. the firm’s consumer product analyst Bonnie Herzog sees the company’s smokeless and traditional cigarette product lines as powerful assets, and writes of the stock, “We see a very compelling set-up for the stock this year given the robust compounding effect of iQOS, PM’s hugely cash-generative combustible cig portfolio and its promising investments beyond nicotine… We believe that PM’s earnings visibility and momentum will hold strong throughout the year, especially given upside potential from a broader & more aggressive global rollout of ILUMA, an accelerated RRP (reduced risk product) innovation pipeline, and increased penetration of iQOS/accelerated user acquisition in lower-income markets driven by further price segmentation… PM remains one of our top stock picks.”

Herzog goes on to give the shares a Buy rating with a $122 price target to imply a 27.5% upside in the coming months. (To watch Herzog’s track record, click here)

Philip Morris stock holds a Strong Buy consensus rating from the Street’s analysts, and it is unanimous, based on 7 recent positive ratings. The shares are trading for $95.68 and their $116.71 average price target suggests a one-year upside potential of 22%. (See PM stock forecast)

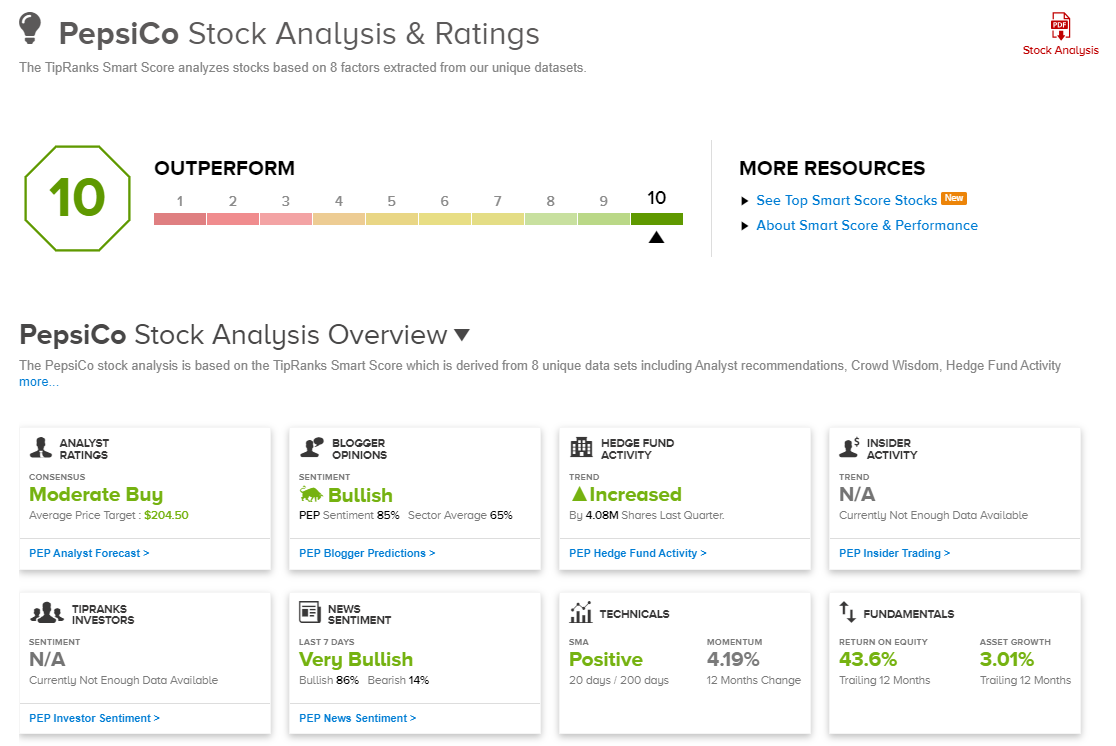

PepsiCo, Inc. (PEP)

Next up is another familiar name in consumer products, PepsiCo, the famous cola challenger to Coke. In addition to its line of Pepsi beverages, the company’s brands, more than 500 in all, include Doritos, Gatorade, SodaStream, and Cheetos, to name just a few.

PepsiCo has a global footprint, with strong market positions in Latin America, Europe, the Asia-Pacific region, and North Africa and the Middle East. The company has a long and successful record of adjusting product lines to match local preferences – just ask Canadians about their Lay’s dill pickle flavored potato chips – and from its New York State headquarters, the company oversees a food and beverage empire that generated over $86 billion in total revenues last year.

More recently, PepsiCo beat the quarterly forecasts in its 2Q23 report. The company’s revenue total, at $22.3 billion, was up almost 10.4% y/y and was $590 million better than had been anticipated. PepsiCo’s earnings, a non-GAAP core EPS of $2.09, was 13 cents better than the estimates.

Even better, looking ahead, for the second time this year, the company raised both its top-and bottom-line guide for FY2023, anticipating 10% revenue growth (vs. 7% beforehand) and 12% core constant currency EPS growth (compared to the previous 9%).

It’s a solid foundation for a consumer staple stalwart, and PepsiCo’s generally strong position is what attracts Goldman’s Herzog. The consumer goods expert writes of this company, “We continue to believe PEP is one of the best-positioned companies across the global food & bev landscape to deliver outsized growth over the next decade based on our in-depth global category growth analysis given their advantaged exposure to snacking and to developing & emerging markets despite what is likely more modest growth (vs the prior decade) across the industry as inflation-led pricing continues to fade. As a result, we believe PEP is poised to drive sustainable long-term topline growth at the high end, possibly exceeding the company’s long-term algo – which we think should be viewed favorably by investors. PEP remains one of our top stock picks.”

In line with her sanguine view of PEP, Herzog gives the shares a Buy rating with a $212 price target that indicates potential for a 21% gain on the one-year time frame.

The 13 recent analyst reviews on PEP shares break down 9 to 4 in favor of Buys over Holds, for a Moderate Buy consensus rating. The stock has an average price target of $204.50, implying a 17% upside potential from the share price of $175.32. (See PepsiCo stock forecast)

Warner Bros. Discovery (WBD)

Wrapping up, we’ll look at Warner Bros. Discovery, a major name in the world’s entertainment industry. This company is the modern embodiment of the storied Warner Bros. company, and counts the brand’s library of famous movies among its assets. WBD entered its current incarnation in April of 2022, when TimeWarner merged with Discovery, Inc. The company brought in $33.8 billion in revenues last year, and boasts a market cap over $28 billion.

All of this is built on a sound platform of entertainment assets. In addition to the legacy Warner Bros. cartoons and movies, WBD can claim ownership of DC Studios; DC Entertainment, the publisher DC Comics; HBO and CNN; and the cable channels brought to the merger by the Discovery Channel. The company’s offerings include something for nearly every viewer, from sports and news to food and cooking shows to superhero movies and gaming. The entertainment portfolio is wide-ranging and diverse, and gives WBD a leadership position as a global media distributor.

Looking at results, we find that Warner Bros. Discovery had 2Q23 revenues of $10.36 billion. While this was up 5.4% y/y, it missed expectations by some $80 million. The company’s bottom line was reported as a GAAP EPS loss of 51 cents per share. This was a notable improvement from the $1.50 EPS loss registered in the prior-year quarter, but was still 10 cents deeper than had been forecast. Positively, free cash flow (FCF) was expected to come in under $1 billion, but came in some distance above that, at $1.7 billion.

That strong metric partly informs Goldman analyst Brett Feldman’s positive thesis, who, despite the earnings miss in Q2, sees plenty to like here. Feldman writes, “We see WBD’s solid 2Q23 report as supporting our outlook for material EBITDA growth, strong FCF generation, and rapid delevering during the remainder of 2023 and through 2024, driven by synergies that are trending ahead of plan and improved go-to-market execution. As such, WBD remains our top pick in Media.”

For Feldman, this adds up to a Buy rating on the stock, and his $20 price target points toward an upside potential of 73% in the next 12 months. (To watch Feldman’s track record, click here)

Overall, this stock has picked up 10 recent analyst reviews, including 7 Buys and 3 Holds, for a Moderate Buy consensus rating. The $11.56 current trading price and $20.88 average price target combine to predict a potential one-year gain of 80.5%. (See WBD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

:quality(85):upscale()/2024/11/13/919/n/1922564/cc0839716735141c6dab05.65024797_.jpg "Best Puffer Coats and Jackets For Women")

:quality(85):upscale()/2024/11/13/790/n/1922564/c0ad2b806734e8c87b1ee9.61099793_.jpg "Best Early Black Friday Fashion Deals 2024")

![Finesse2Tymes & Og Boo Dirty – Real Recognize Real [Official Music Video]](https://i.ytimg.com/vi/3xb4bl5PWF8/maxresdefault.jpg "Finesse2Tymes & Og Boo Dirty – Real Recognize Real [Official Music Video]")

")

| Vevo")

")