Nvidia has been one of the top-performing stocks on the market in the past year with outstanding gains of 215%, which is not surprising as the company has absolutely dominated the market for artificial intelligence (AI) chips and witnessed remarkable growth in its revenue and earnings.

However, there is one business where Nvidia is still lacking. The company’s revenue from the automotive segment stood at $1.1 billion in fiscal 2024, an increase of 21% over the previous year. The segment turned in a tepid performance in the final quarter of the fiscal year, with a year-over-year decline of 4% in revenue to $281 million.

Nvidia has been trying to make a dent in the market for automotive chips for a very long time, once boasting customers such as Tesla. However, Nvidia has failed to make it big in this business so far. The automotive chip market was worth an estimated $51 billion last year, becoming the third-largest end market for chips.

Nvidia’s automotive revenue last year indicates that it has managed to capture just 2% of this market, which may seem a tad surprising as the company is known to dominate the markets in which it operates. However, there is one company that’s making solid progress in the automotive chip market and seems set to become a key player in this space in the future — Qualcomm (NASDAQ: QCOM).

Let’s look at the reasons why the automotive market could give Qualcomm a nice boost.

Qualcomm’s automotive chip pipeline is expanding at an impressive pace

In the second quarter of fiscal 2024 (which ended on March 24), Qualcomm posted $603 million in automotive revenue, up an impressive 35% from the year-ago period. It is worth noting that the chipmaker’s automotive revenue grew at a faster pace than its overall revenue, which was up just 1% year over year to $9.38 billion.

The automotive business accounted for 6.5% of Qualcomm’s total revenue in the previous quarter. While that’s not very significant, investors should note that the automotive business produced 4.8% of its top line in the same period last year. More importantly, this segment seems set to drive the needle in a more meaningful way for the company.

That’s because Qualcomm exited the previous quarter with an automotive design win pipeline of $45 billion. A design win means that Qualcomm’s automotive chips have been selected for deployment by automakers or original equipment manufacturers (OEMs), and they should translate into revenue once those products go into production.

The company has generated $1.2 billion in automotive revenue in the first six months of the current fiscal year, a 33% increase over the same period in the preceding year. So, Qualcomm’s six-month automotive revenue is greater than what Nvidia generated from this segment in the previous fiscal year. Additionally, Qualcomm management is confident that its automotive business will keep growing at a faster pace than the end market, suggesting that the company is on track to gain more share.

Third-party estimates predict that the automotive chip market could clock annual growth of over 10% through 2032 and generate annual revenue of $128 billion. So, management’s claim that Qualcomm is growing at a much faster pace than the end market indeed stands true. Moreover, Qualcomm’s automotive pipeline has increased by 50% in the space of 18 months since its automotive investor day was held in September 2022.

This sales funnel could continue improving, given the secular growth opportunity present in the automotive chip market, as well as the fact that Qualcomm is providing an end-to-end platform that enables multiple functionalities such as digital cockpits, automated driving, and cellular connectivity, among others.

The stock is set for healthy gains

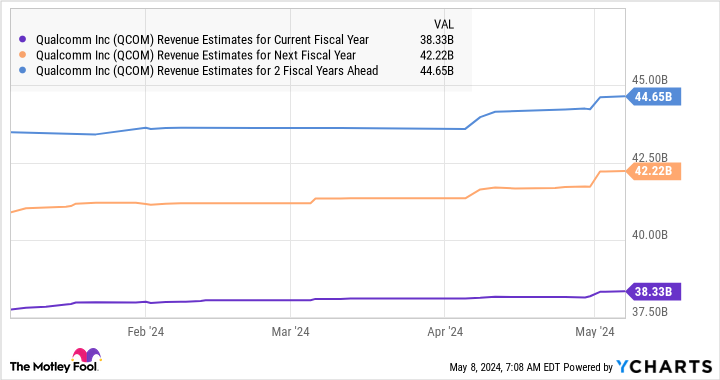

Qualcomm is expecting the automotive business to generate more than $4 billion in annual revenue by fiscal 2026. That would be more than double the $1.87 billion revenue the company generated from this segment in fiscal 2023, translating into a three-year revenue growth rate of 29%. Thanks to the impressive growth the company has been logging in markets such as automotive, analysts have raised their growth expectations for Qualcomm.

QCOM Revenue Estimates for Current Fiscal Year Chart

The fiscal 2026 revenue estimate of $44 billion suggests that the automotive business could account for 10% of the company’s top line in a couple of years, based on Qualcomm’s $4 billion revenue expectations. Also, the $45 billion pipeline is an indication that the segment will become a bigger contributor to the company’s business in the long run.

Assuming Qualcomm does hit $44.6 billion in revenue in fiscal 2026 and trades at 7 times sales at that time, in line with the U.S. Technology Sector’s sales multiple, its market cap could increase to $312 billion. That would be a 55% jump from current levels. Qualcomm is currently trading at 5.5 times sales, which is a discount to the tech sector.

The acceleration in automotive and AI-related catalysts in the smartphone market could lead the market to reward Qualcomm with a higher earnings multiple, which could potentially lead to more upside than what’s predicted in the previous paragraph. That’s why investors looking for a growth stock should consider buying Qualcomm right away, as it has multiple catalysts, and it is way cheaper than peer Nvidia, which currently trades at an expensive 37 times sales.

Should you invest $1,000 in Qualcomm right now?

Before you buy stock in Qualcomm, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Qualcomm wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $550,688!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 6, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia, Qualcomm, and Tesla. The Motley Fool has a disclosure policy.

Missed Out on Nvidia? This Incredibly Cheap Semiconductor Stock Is Crushing Nvidia in a Key Market Right Now, and It Could Soar 55%. was originally published by The Motley Fool

:quality(85):upscale()/2024/11/13/790/n/1922564/c0ad2b806734e8c87b1ee9.61099793_.jpg "Best Early Black Friday Fashion Deals 2024")

| Vevo")

")

")

")