Enthusiasm around artificial intelligence (AI) has played a big role in pushing the markets higher so far this year. Although big tech stocks such as Nvidia and Microsoft have witnessed outsize buying activity, many investors have been looking at less obvious choices in hopes of identifying the next big AI opportunity.

One such company that has experienced its share of hype is Super Micro Computer (NASDAQ: SMCI). Shares of the AI darling are up 234% over the last year, and 218% just in 2024.

While Supermicro has been closely affiliated with Nvidia, the underlying business is actually quite different — and in my opinion, I think it’s far less lucrative.

Let’s dig into the investment prospects of Supermicro and explore if the stock deserves a spot in your portfolio.

Supermicro’s business is soaring, but…

Perhaps the hottest pocket of the AI realm is semiconductors. Demand is soaring for graphics processing units (GPUs) as generative AI applications continue to evolve.

For now, Nvidia, AMD, Intel, and some other chip designers have emerged as the biggest names in the GPU market. While Supermicro is works with many chip companies, it’s not a semiconductor company itself.

Rather, Supermicro specializes in IT infrastructure. Essentially, the company designs architecture solutions such as storage clusters for high-performance GPUs.

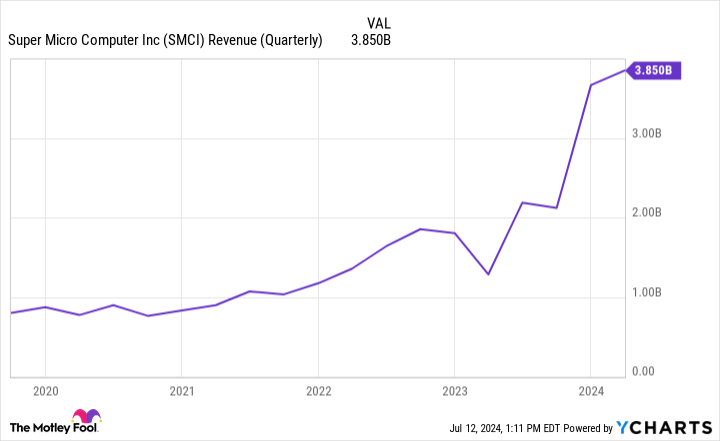

The revenue trends seen below illustrate how the heightened demand and buying activity surrounding chips has served as a bellwether for Supermicro’s services over the last couple of years.

While the newfound revenue growth is encouraging, there are some lowlights investors should be aware of when it comes to Supermicro.

SMCI Revenue (Quarterly) Chart

…there is more than meets the eye

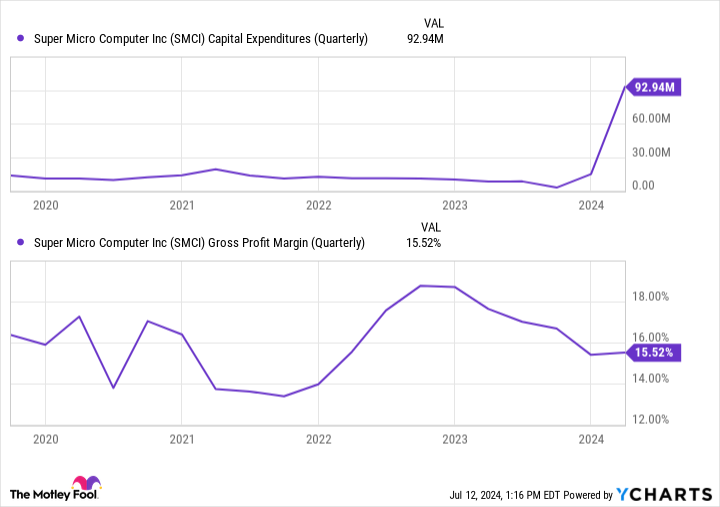

While rising demand can be considered a good thing for Supermicro, keep in mind that building IT infrastructure is an expensive business.

Take a look at the dynamics in the charts below. In more recent quarters, Supermicro’s capital expenditures (capex) have ballooned. The idea I’m trying to convey here is that while the company’s revenue is surging, expenses are also rising significantly.

This dynamic is directly impacting Supermicro’s margin profile. As observed below, Supermicro’s gross margin is actually plateauing at the moment.

SMCI Capital Expenditures (Quarterly) Chart

Admittedly, the financials analyzed above aren’t necessarily a reason to run for the hills. However, there are a couple of other potential issues to explore as they relate to Supermicro.

Keep in mind that the semiconductor space is a cyclical industry. Right now, chip businesses are enjoying a bit of a renaissance fueled by AI euphoria. But like any other type of business, eventually supply and demand trends will normalize.

That could spell trouble for Supermicro in the long run. It’s pretty difficult to forecast demand for any product, let alone cutting-edge chips that are used for breakthrough applications in AI. Those themes have me concerned that Supermicro’s business may witness a deceleration. This could further impact the company’s profitability profile, which would be an unwelcome surprise given the already low-margin nature of the business.

Image source: Getty Images.

Is now a good time to buy Supermicro stock?

While many investors have undoubtedly made a lot of money owning Supermicro stock, I’m skeptical that the returns were for the right reasons. I am suspicious that many investors see Supermicro as analogous to Nvidia and have poured into the stock accordingly. Therefore, when Nvidia and other chip stocks begin trading upwards, shares of Supermicro have followed.

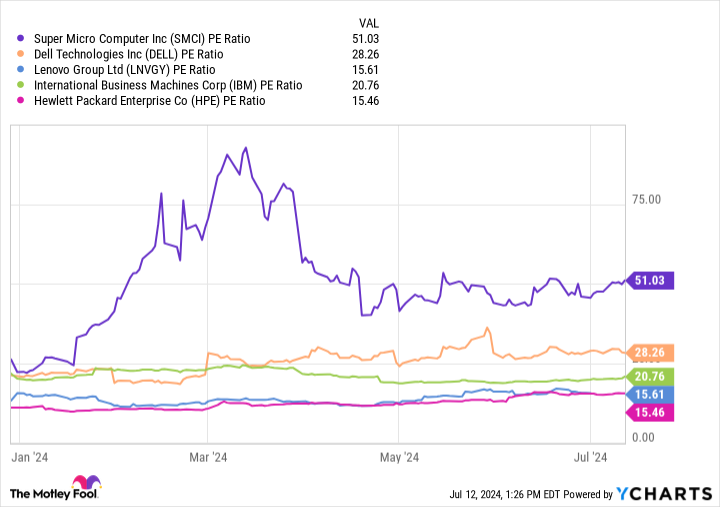

SMCI PE Ratio Chart

The chart above benchmarks Supermicro against a peer set on a price-to-earnings (P/E) basis. The obvious takeaway from the valuation trends above is that Supermicro is valued at a significant premium to its peers.

However, a more subtle argument is that businesses such as Dell Technologies and International Business Machines in particular are not only much larger than Supermicro, but they are far more diversified when it comes to products and services. And yet Supermicro’s P/E is more than double that of IBM and meaningfully higher than Dell’s.

Considering the level of competition and the cyclicality of the chip space more broadly, mixed with the high capex and low-margin nature of Supermicro’s business, I can’t help but think the stock is overvalued.

I think investors with a long-term horizon have better opportunities in the chip space and the AI arena in general. While scooping up Supermicro stock looks tempting, I see the company as more of trade and less of an investment.

Should you invest $1,000 in Super Micro Computer right now?

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $791,929!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 8, 2024

Adam Spatacco has positions in Microsoft and Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Microsoft, and Nvidia. The Motley Fool recommends Intel and International Business Machines and recommends the following options: long January 2025 $45 calls on Intel, long January 2026 $395 calls on Microsoft, short August 2024 $35 calls on Intel, and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Is Super Micro Computer Stock a Good Buy Right Now? was originally published by The Motley Fool

")

")

")

")

![Nicki Minaj & Ice Spice – Barbie World (with Aqua) [Official Music Video]](https://i.ytimg.com/vi/CUj2AWEJnwQ/maxresdefault.jpg "Nicki Minaj & Ice Spice – Barbie World (with Aqua) [Official Music Video]")