Microsoft, Amazon, and Alphabet are very different companies, but they are the top three players in the fast-growing cloud computing industry.

They offer hundreds of cloud services to businesses, from simple data storage to complex software development tools. More recently, they have invested heavily in new data centers filled with powerful graphics processors (GPUs) from the likes of Nvidia, and they rent the computing power to artificial intelligence (AI) developers. This could be one of the most valuable opportunities in the history of the cloud industry.

Microsoft, Amazon, and Alphabet are locked in a fierce battle for AI market share. DigitalOcean (NYSE: DOCN), on the other hand, has carved out a lucrative niche by only serving small and mid-sized businesses (SMBs), which are often overlooked by its trillion-dollar competitors. DigitalOcean stock looks like a great value, and here’s why investors might want to buy it right now.

Image source: Getty Images.

Democratizing access to AI infrastructure

The cloud leaders typically focus on serving large organizations because they have the highest budgets, whereas SMBs receive less attention. DigitalOcean targets those customers exclusively, whether they are in the start-up phase or they have up to 500 employees.

DigitalOcean provides them with highly personalized service, clear and transparent pricing, and cloud tools that are simple to deploy, because the company knows most of its customers can’t afford in-house technical teams.

DigitalOcean is now using that blueprint to deliver affordable AI solutions to customers. Right now, cloud leaders let their largest customers access tens of thousands of GPUs worth of computing capacity, which means developers with significant financial resources are building the most advanced AI models. Smaller companies simply can’t compete.

DigitalOcean recently announced it will allow its customers to access small numbers of AI GPUs (typically between one and eight), including Nvidia’s flagship H100, to integrate AI into their workflows at a scale that suits them. CEO Paddy Srinivasan says this fractional on-demand access to GPUs is a first of its kind for the industry, and it helps democratize access to AI.

The company will also open a new state-of-the-art data center in Atlanta in early 2025 that will expand its AI compute capacity. It adds to the capacity DigitalOcean acquired when it bought Paperspace last year, which is a specialist in delivering AI data center infrastructure at affordable rates.

In fact, Paperspace is up to 70% cheaper than cloud leaders like Microsoft Azure when it comes to AI compute capacity, because it offers per-second billing to reduce wastage, and it doesn’t lock customers into contracts. Plus, it has a leaner cost structure because it offers a narrow set of services, and it passes those savings on to the customer.

DigitalOcean’s revenue growth is reaccelerating

DigitalOcean generated a record $192.5 million in revenue during the second quarter of 2024 (ended June 30), which was a 13% increase from the year-ago period. It marked the second consecutive quarterly growth acceleration.

The company was regularly growing its top line by more than 30% each quarter just two years ago, so it has slowed considerably overall. One reason is that DigitalOcean is currently slashing costs in order to boost its profitability. During Q2, the company had total operating expenses of $95 million, which was an 8.5% reduction from the year-ago period.

That resulted in $19.1 million in net income, a whopping 2,777% increase.

The fact DigitalOcean managed to accelerate its revenue growth while cutting costs and generating a healthy profit really speaks to the organic demand for its cloud services.

Plus, here’s something investors should keep an eye on in the coming quarters. DigitalOcean said its revenue attributable to AI, specifically, soared by a staggering 200% year over year in Q2. The company didn’t disclose how much revenue it actually generated from its AI services (including Paperspace), so we can assume that growth was from a very low baseline number — but it still signals surging demand.

Why DigitalOcean stock is a buy now

According to an estimate by Grand View Research, the cloud industry overall will be worth around $730 billion this year. The SMB segment alone could be worth $114 billion according to DigitalOcean, but the company expects it to grow by 23% annually going forward compared to just 21.2% for the cloud industry overall.

DigitalOcean’s strategy to deliver affordable AI infrastructure and services could add a new dimension to that opportunity, because it’s penetrating a brand new market that has been underserved by other providers. Global consulting firm PwC thinks AI will add $15.7 trillion to the global economy by 2030, so it’s easily the largest financial opportunity DigitalOcean has faced to date.

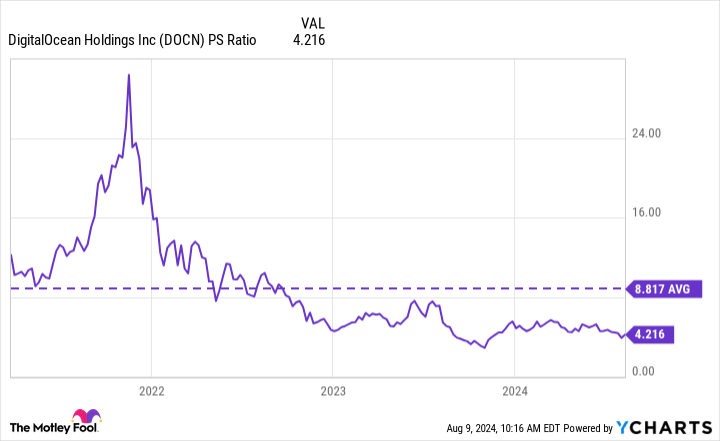

DigitalOcean stock is currently trading 75% below its all-time high that was set during the tech frenzy in 2021. It was overvalued back then with a price-to-sales (P/S) ratio of around 30, but the company has grown its revenue consistently ever since, and its P/S ratio now stands at just 4.1.

That’s more than a 50% discount to its average P/S ratio of 8.8 going back to when the company came public in 2021:

DOCN PS Ratio Chart

Simply put, DigitalOcean stock looks like a good value right now. Combine that with the company’s accelerating revenue growth, surging profitability, and enormous opportunities in the cloud and AI industries, and investors could do well to start buying.

Should you invest $1,000 in DigitalOcean right now?

Before you buy stock in DigitalOcean, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and DigitalOcean wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $641,864!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 12, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, DigitalOcean, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

If You Like Microsoft, Amazon, and Alphabet, You Might Love This Growth Stock was originally published by The Motley Fool

")

![Gucci Mane & Sexyy Red – You Don’t Love Me [Official Music Video]](https://i.ytimg.com/vi/j7IBqyFKT4c/maxresdefault.jpg "Gucci Mane & Sexyy Red – You Don’t Love Me [Official Music Video]")

| Vevo")

")